In its latest report, Kline forecasts volume growth in the global lubricants market to remain essentially flat for the foreseeable future. While that may have been expected, George Morvey, Kline’s Energy Industry Manager, says that what might be less apparent is how suppliers must look even more closely for key indicators of change to seize the increasingly elusive niche opportunities that remain.

In its latest report, Kline forecasts volume growth in the global lubricants market to remain essentially flat for the foreseeable future. While that may have been expected, George Morvey, Kline’s Energy Industry Manager, says that what might be less apparent is how suppliers must look even more closely for key indicators of change to seize the increasingly elusive niche opportunities that remain.

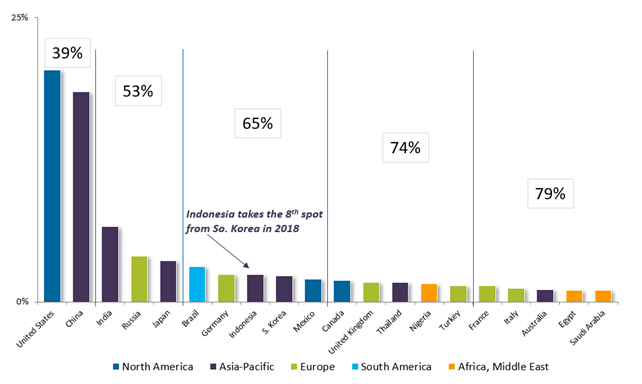

Market overview

In 2018, the global demand for finished lubricants reached 40.5 million tonnes, with automotive oil products accounting for over 50% and Asia-Pacific taking 44% of finished lube volumes. The two largest markets, the United States and China, accounted for 39%, which means these countries still have the biggest impact on product trends, viscosity grade evolution, supplier positioning, synthetics penetration, and channel shifts.

Estimated Finished Lubricant Demand in the “Top 20” Leading Country Markets, 2018

However, a number of industry trends including trade tensions, economic pressures, increased vehicle electrification, and a growing use of synthetics are continuing to suppress volumetric growth. As a result, Kline forecasts a global finished lubricant demand growth at a CAGR of 0.4% over the next 10-year period.

On the quality side, there is a growing demand for high-performance, lower-viscosity products. In passenger car applications, for example, SAE 0W and 5W grades are expected to account for 26% of total demand by 2028. In the same timeframe, in the commercial vehicle sector, SAE 15W-40 demand looks set to hold at 47%, SAE 10W grades are expected to reach 20%, and monogrades will rapidly exit the market.

Changing market opportunities

In such a lackluster market, Kline’s Energy Practice is regularly asked about volumetric lubricant demand growth and to help identify which country markets offer opportunities for lubricant suppliers. In the not-too-distant past, emerging and developing country markets were rapidly growing in terms of lubricant demand, and suppliers could ride the wave and build volume. As we look ahead, those opportunities seem to be few and far between.

One of the key trends impacting these markets is the introduction of government initiatives that aim to limit imports in a drive toward self-sufficiency. In Russia, for example, an import substitution policy has been implemented with the end goal of limiting the import of finished lubricants, especially synthetics, while encouraging consumers to support domestic Russian suppliers. Similar issues are evident in India and China, where the “Make in India” and “Made in China 2025” initiatives aim to help local and state-owned manufacturers provide their products to consumers. These initiatives offer stiff competition to international players and create competitive disadvantages and barriers to entry for organizations without a local presence.

It is now more important than ever for lubricant suppliers to focus on identifying and monitoring trends at, or just below, the surface across the globe to be on the right side of the demand wave going forward. In-country primary research conducted by Kline’s Energy Practice team is one way to monitor initiatives and market trends that will power future lubricant demand.

Exploring opportunities in the Philippines

In the commercial automotive market segment, which includes on- and off-highway sectors, market change tends to occur relatively slowly. This means suppliers should look closely for key indicators of change and quickly react to claim their share of the resulting demand. This is no more evident than in the Philippines.

The country, for the most part, supports an old vehicle parc with significant demand for monograde heavy-duty motor oil (HDMO). Used vehicles from neighboring countries are routinely imported into the Philippines, continuing the cycle of high monograde demand. This, in turn, means the continued use of obsolete API service categories, low penetration of synthetics, and limited consumer brand awareness and loyalty to a particular supplier.

However, there are several initiatives and market trends that may increase demand for lubricants in the country over the next five to 10 years.

Infrastructure development

The Duterte administration’s Build, Build, Build economic project for infrastructure development will primarily benefit the construction segment. The program is planned to increase spending on infrastructure from 5.4% of GDP in 2017 to 7.3% by the end of 2022. Seventy-five projects are planned, including airports, railways, bus rapid transits, roads bridges, and seaports, of which the National Economic Development Authority expects some 28 to be completed by 2022. The associated growth in construction activities and the rise in demand for construction equipment can be expected to drive demand for commercial lubricants.

Growth of ride-hailing services

Along with the metered taxis operating in urban areas, the number of private taxis and app-based ride-hailing platforms, such as Grab and Uber, is growing. This is particularly the case in the major cities such as Metro Manila and Cebu. The trend is mainly due to the lack of an adequate public transportation system and is expected to positively impact commercial lubricant demand, as more and more vehicles are added to the fleets of ride-hailing service companies.

Public Utility Vehicles (PUV) modernization

Older jeepneys and buses will be phased out.

The Land Transportation Franchising and Regulatory Board (LFTRB) and the Department of Transport (DOTr) plan to modernize jeepneys, which have been the most popular means of public transportation in the country. This will be achieved under the Public Utility Vehicle Modernization Program (PUVMP), which features a regulatory reform and new guidelines for the issuance of franchises for road-based public transport services. The program mandates the phasing out of jeepneys and buses aged 15 years and older and the replacement of non-Euro 4 compliant engines with new models. These new engines will likely have OEM engine oil recommendations for current API service category products and enable both longer oil drain intervals and the use of lower viscosity grades.

These are select examples of government and industry initiatives designed to spur economic growth, provide employment, and offer economical and environmentally friendly public transportation options to the general population. Their potential to drive demand for finished lubricants is researched and presented as part of Kline’s new global lubricants report.

New report highlights growth opportunities

To succeed in this low-growth market, lubricant suppliers will need reliable, in-depth insight into the potential growth markets so that they can seize any opportunities that do arise. The latest Global Lubricants: Market Analysis and Assessment provides a comprehensive analysis of automotive and industrial finished lubricant products, end-use industries, trade classes, major suppliers, and market trends in leading markets.

The report covers 20 country profiles and analyses covering niche markets including Indonesia, Chile, and, for the first time, Ghana and Kenya.

To read more about the Global Lubricants: Market Analysis and Assessment report, to request a sample, or to purchase a copy, please visit our website.